To understand the UX challenges facing legacy and challenger banks lets first go back to August 2020. When the New York branch of Citibank were instructed by its client, Revlon, to send interest payments totalling $7.8 million to their creditors. Revlon wanted to refinance its debt and roll most of the debt onto a new loan, a standard request and nothing extraordinary.

However, what actually happened was that the banker at Citibank paid the all the creditors in full, with interest.

- The amount? $500 million.

- The cause? Bad UX.

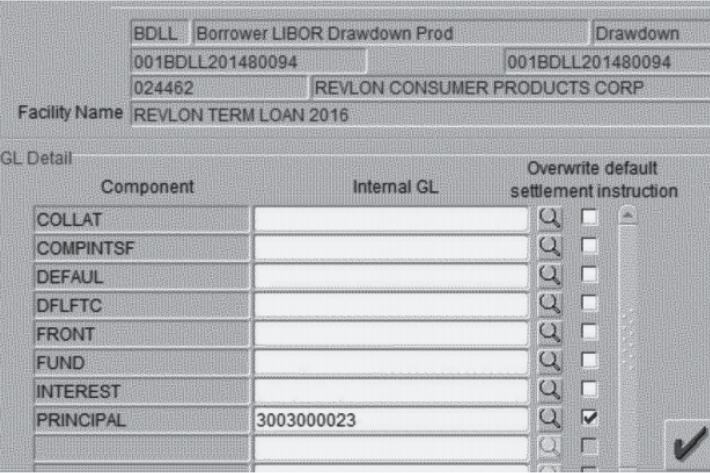

The bank was working on the Flexcube platform – not just an unattractive interface, but one that was lacking in any considered UX design.

A quick investigation highlighted that to prevent the whole $500 million being paid, the banker needed to have ticked the ‘front’, ‘fund’ and ‘principal’ boxes in the antiquated form, and the account number needed to have been added to each. For a sum of this size, Citibank require a three-person check. In this case, a subcontractor, a colleague of his in India, and a senior at Citibank all thought that just the ‘principal’ box needed the account number.

The result?

In a landmark case, a judge ruled in favour of the creditors who had all taken a share of the $500 million and Revlon would never see that money again. A very costly mistake which, in retrospect, could have been avoided through a now common UX feature that notifies users of a cash transfer: ‘Are you sure you want to make a $500 million transfer?’

While this is an extreme case, it does highlight the fundamental importance of UX in finance. More day-to-day examples could be the customer who leaves as they can’t create a payee on their mobile – or functions such as blocking a card or not being able to access live support.

UX Challenges experienced by both Legacy banks and challenger banks:

It’s widely understood that consumers have never had so many choices when deciding on who to bank with. Until recently, retail banking has been done mostly with legacy banks – household names we all grew up with like Santander, NatWest, Barclays and Lloyds.

They’ve an established track record in managing money, providing mortgages, credit and debit services and a range of products thatare easily adopted by loyal customers. Notwithstanding the 2008 financial crash, ‘legacy banks’ still have a distinguished reputation and remain trusted by hundreds of millions of people globally and despite the meteoric rise of challenger banks, four out of every five transactions are handled by legacy banks.

However, from a UX and broader CX perspective, many struggle and are feeling the pain.

A recent review of legacy banks by Build for Mars, found that consumers are still not able to set up an account through the app, are slow to fixing IT issues, integrated communication channels, and tend to favour call centre support in favour of live chat functionality. Another pain point cited by users was the lack of software updates that introduce new features, poor log-on times and worst of all – hidden fees, mostly when transferring money abroad.

Enter: The challenger banks…

This is in large part why many consumers are moving to challenger banks. A review of the challenger bank market by Beauhurst found that in 2022, of the UK’s current unicorn companies, one in two were FinTech’s, including four of the biggest challenger banks – Revolut, Monzo, Starling Bank and OakNorth (all headquartered in London). Moreover, despite FinTech being a relatively nascent industry, UK challenger banks have raised nearly £7 billion worth of investment, across 149 equity deals, since 2011. Nearly £1 billion of this has been invested since 2020 – a sign that the challenger bank market is growing rapidly.

However, challenger banks are not without their own UX issues. While they might be a more convenient method of banking, typically with excellent customer support, and improved user functionality, they lack one key ingredient that is arguably the most important feature that consumers want in their banks: trust. Trust that legacy banks have spent decades in building. People typically trust legacy banks much more than they do challenger banks.

A recent report by IBM found that the biggest challenge facing financial institutions is how to redefine and earn customers’ trust. This has been exacerbated by the Covid-19 pandemic and the current cost of living crisis that many people in the UK are facing, and there is no getting away from the fact that the people typically trust legacy banks much more than they do challenger banks.

Building trust is one of the cornerstones of good UX and yet it is intangible, hard to define and even harder to measure.

UX challenges – support is at hand.

ExperienceLab is an international human-centred design and insight agency, founded within the National Physics laboratory more than 20 years ago. We’ve been putting users at the centre of great design ever since – building trust for brands through engaging products that make the world better designed for everyone. We continue to support several FSI brands to help them understand their UX issues, using a series of UX methodologies to help them to build a more modern user experience. We worked with a global charge and credit card provider to test and prototype UX options for Membership rewards card holders and when an FX leading company needed insight into users’ challenges, we delivered rounds of usability testing to ensure that every button click and screen option was intuitive and seamless.

What next?

If you’re are a legacy bank looking to freshen up and improve your UX, or a challenger bank looking to build trust and integrity through sound UX methods, or come from any sector in the FSI spectrum, get in touch and let us share some initial ideas and walk through case studies where we’ve empowered similar brands to build trust, recruit and retail clients and expand their digital products in a connected and joined-up way.